The $4.8M Engagement That Went Wrong

A $4.8M Murex transformation failure is not an isolated case; it reflects a structural hiring gap in capital markets engineering. Upgrading MX.3, configuring structured products, and meeting regulatory mandates like CFTC reporting require deep front-office expertise not just generic Murex exposure.

Hiring Murex & Capital Markets Platform Engineers from India has become a strategic priority for global banks looking to scale efficiently. But the gap between back-office experience and real front-office, asset-class-specific capability is where most programs fail leading to pricing errors, compliance risks, and costly rebuilds.

The urgency is accelerating with rising technology investment. According to Gartner, global IT spending is projected to reach $6.15 trillion in 2026, growing 10.8% year-over-year, driven heavily by AI infrastructure, trading systems, and enterprise platform modernization: Gartner IT Spending Forecast 2026

In this environment, success depends not on hiring more engineers but on hiring specialists with proven MX.3, front-office, and regulatory implementation depth from day one.

TL;DR 8 Answers Before You Read Further

| Question | Answer |

| What does a Senior Murex Developer cost from India? | $72–110/hr fully loaded. A Murex Functional Architect runs $130–170/hr. Section 5 has the full rate stack. |

| Which Indian city has the deepest Murex talent? | Gurgaon and Mumbai. Both cities have capital markets GCC concentration. Gurgaon for front office and derivatives. Mumbai for fixed income and regulatory. |

| Fastest I can close 10 Murex engineers? | 45–65 days with a pre-vetted bench. 90+ days sourcing cold. Murex is the thinnest pool in India enterprise staffing at senior level. |

| What's the most important thing to verify before interviewing? | Asset class and desk coverage front office vs back office, and which instrument types specifically. A Murex developer with FX settlement experience is not a Murex developer for a rates structured products desk. |

| What certification actually matters for Murex? | Murex has no public certification program. Experience verification is entirely interview and reference dependent. Section 7 covers the only reliable verification method. |

| How many senior Murex architects are actually available in India? | Approximately 180 Murex architects with front office and complex derivatives experience are active in India. The total Murex-experienced pool is approximately 3,800 but most are back-office or settlement focused. |

| What's typical attrition for Murex specialists? | 8–12% annually. The lowest attrition of any enterprise stack in India. Murex specialists have very few lateral options; the community is small and the skill is non-transferable to other platforms. |

| What's the biggest hiring mistake for capital markets programs? | Treating "Murex experience" as a single qualification. Front office, middle office, back office, and regulatory are different Murex skill sets requiring different practitioners. Section 5 explains the distinction in full. |

Are You Actually Ready for This?

Capital markets platform engagements are among the most complex in enterprise technology. The failure consequences of regulatory exposure, trading desk P&L impact, and settlement failures are more severe than almost any other program type. Score yourself before you engage a vendor.

Score each: 0 (not in place), 2 (partially), 4 (done).

| # | Criterion | Score |

| 1 | Named program owner with capital markets domain knowledge. Not just a delivery manager. | 0/2/4 |

| 2 | Asset class scope defined which instruments, which desks, which markets | 0/2/4 |

| 3 | MX.3 version confirmed current version and target version if upgrading | 0/2/4 |

| 4 | Front office vs middle office vs back office scope separated these require different profiles | 0/2/4 |

| 5 | Regulatory reporting requirements confirmed CFTC, EMIR, MiFID II, SFTR, or combination | 0/2/4 |

| 6 | Integration scope documented which upstream and downstream systems connect to Murex | 0/2/4 |

| 7 | Interview panel with hands-on Murex experience and asset class knowledge available within 5 business days | 0/2/4 |

| 8 | Legal SLA under 15 days for MSA review | 0/2/4 |

| 9 | Development environment access provisioned for offshore team | 0/2/4 |

| 10 | Model validation process defined who validates pricing model configurations | 0/2/4 |

| 11 | KPIs defined: trade booking accuracy rate, settlement fail rate, regulatory reporting completeness | 0/2/4 |

| 12 | Data confidentiality requirements confirmed which market data, positions data offshore engineers can access | 0/2/4 |

| 13 | Escalation path: vendor PM → your Murex Program Lead → your CTO/COO | 0/2/4 |

| 14 | IP ownership for custom pricing models, workflow configurations, and regulatory mappings in MSA | 0/2/4 |

| 15 | Finance can process USD-denominated invoices within 30 days | 0/2/4 |

What your score means:

| Score | Tier | Reality Check |

| 48–60 | Scaler | You’re ready. This guide is a checklist. |

| 34–46 | Builder | 3–4 gaps. In capital markets, they cost more than time they cost regulatory standing. Fix before signing. |

| 20–32 | Explorer | Significant internal work needed. A premature capital markets engagement creates more risk than it resolves. |

| 0–18 | Pre-Stage | 90 days of internal program definition before an offshore engagement makes sense. |

From the deal floor: A European investment bank €45B AUM, Murex MX.3 for FX and rates scored 18 on this checklist. Their CTO signed a 10-person SOW anyway. The asset class scope had never been documented (criterion 2). The offshore team spent the first 8 weeks in requirements gathering that should have been complete before the SOW was signed. Eight weeks at €85/hr blended across 10 engineers: €272K spent on discovery that was the bank’s homework. The score predicted the outcome.

The Capital Markets Talent Market in India 2026

India is the largest offshore delivery location for capital markets technology globally. Every tier-1 investment bank JPMorgan, Goldman Sachs, Morgan Stanley, HSBC, Barclays, Deutsche Bank, Citi runs significant Murex and capital markets platform engineering from India. That concentration of enterprise delivery has created a talent pool unlike any other technology stack in the country.

The paradox of capital markets talent in India:

The pool is simultaneously large and thin. Largely because India has been delivering capital markets technology for 25+ years TCS, Infosys, Wipro, Cognizant, and specialist firms have built entire practices around Murex, Calypso, and Temenos. Thin because the asset class and desk specialisation within capital markets creates extreme fragmentation.

A Murex developer with 10 years of FX derivatives experience in a tier-1 investment bank GCC is a completely different profile from a Murex developer with 10 years of fixed income back-office experience at a domestic Indian bank. Both describe themselves as “senior Murex developers.” They are not the same profile.

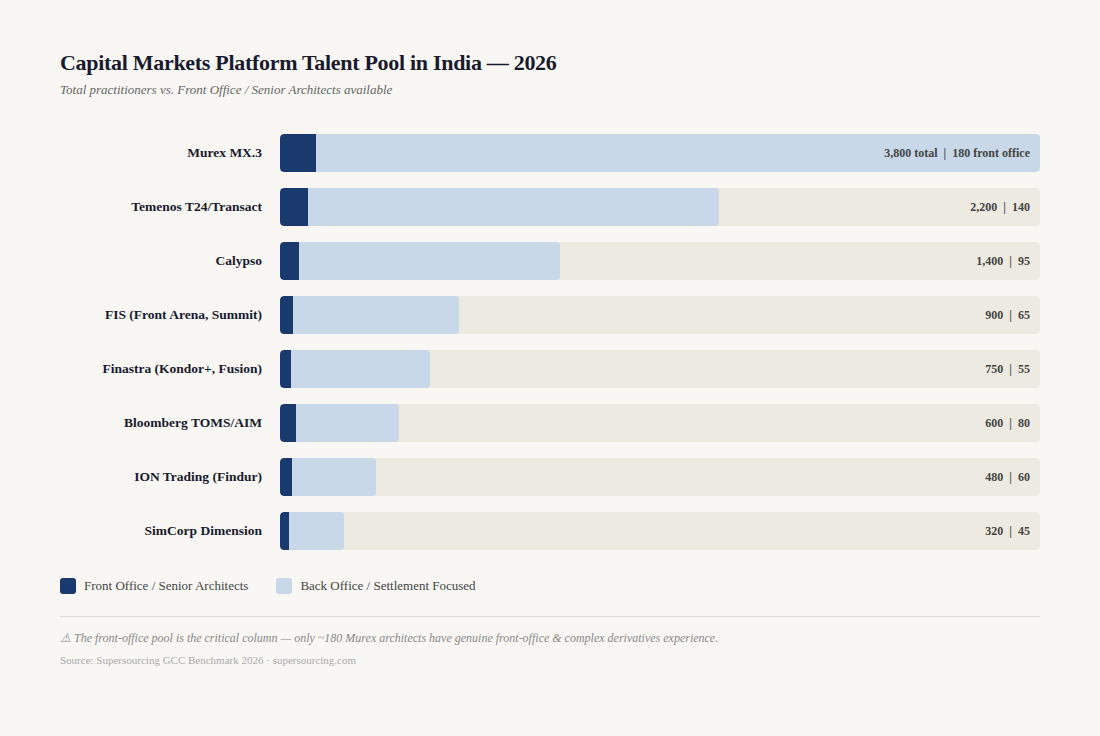

The overall capital markets platform pool:

| Platform | Estimated India Pool | Front Office / Senior Architects | Back Office / Settlement Focused |

| Murex MX.3 | ~3,800 | ~180 | ~3,620 |

| Calypso | ~1,400 | ~95 | ~1,305 |

| Temenos T24/Transact | ~2,200 | ~140 | ~2,060 |

| FIS (Front Arena, Summit) | ~900 | ~65 | ~835 |

| Finastra (Kondor+, Fusion) | ~750 | ~55 | ~695 |

| Bloomberg TOMS / AIM | ~600 | ~80 | ~520 |

| ION Trading (Openlink, Findur) | ~480 | ~60 | ~420 |

| SimCorp Dimension | ~320 | ~45 | ~275 |

The critical column is “Front Office / Senior Architects” ; these are the practitioners who have configured pricing models, built trading workflows for complex derivatives, implemented risk engines, and delivered regulatory reporting for tier-1 programs. The back-office pool is large. The front-office pool is genuinely scarce.

The domestic Indian bank problem:

India has a large domestic banking sector SBI, HDFC, ICICI, Axis, Kotak and many of these banks run Murex, Temenos, or Calypso for their treasury and derivatives operations. Indian domestic banks trade primarily plain vanilla instruments, interest rate swaps, FX forwards, basic options. Their Murex implementations are configured for simple instrument types, domestic regulatory requirements (RBI reporting), and settlement-focused workflows.

A Murex developer from a domestic Indian bank background has genuine Murex experience. They do not have experience configuring MX.3 for exotic derivatives, building front office risk workflows, implementing CFTC/EMIR/MiFID II regulatory reporting, or supporting a trading desk with complex structured products. When vendors say “Murex experience,” a significant proportion of their bench comes from this domestic bank background.

For global capital markets programs, domestic Indian bank experience is a starting point, not a sufficient qualification. Ask specifically: global bank or domestic bank? Which instruments? Which regulatory regimes?

Where the talent lives:

| City | Dominant Capital Markets Specialisations | Why |

| Gurgaon | Murex front office (rates, FX, credit), Calypso, FIS Front Arena, BFSI capital markets | Highest concentration of global investment bank GCCs. JPMorgan, Goldman Sachs, American Express, Capital One all have significant Gurgaon presence. Front office and derivatives depth. |

| Mumbai | Fixed income, Murex back office and regulatory, Temenos treasury, Bloomberg | India’s financial capital. Proximity to NSE, BSE, and domestic banking ecosystem. Strong regulatory reporting depth. RBI compliance-driven implementations. |

| Bangalore | Calypso, Finastra, ION Trading, cloud-native capital markets platforms | Technology-first talent. Stronger on modern API-driven capital markets platforms. Less depth on legacy Murex front office. |

| Pune | Murex back office, settlement, TCS/Infosys capital markets delivery | Large SI delivery centers. Strong in settlement, reconciliation, and back-office Murex programs. Less front office depth. |

| Chennai | Temenos T24/Transact, core banking, legacy capital markets | TCS/Cognizant legacy banking delivery. Deep in core banking and treasury. Less in complex derivatives. |

| Hyderabad | Finastra Fusion, Microsoft Azure capital markets integration, ITSM for financial services | Microsoft ecosystem integration for financial services. Growing Finastra presence. |

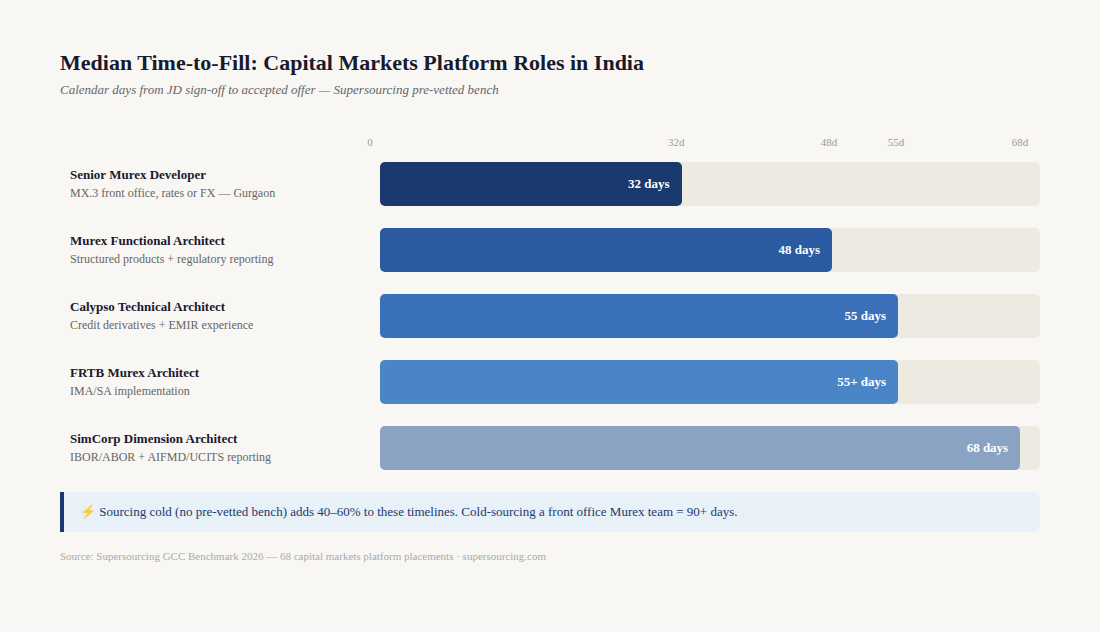

Supersourcing Index: Across 68 capital markets platform placements in the Supersourcing GCC Benchmark 2026, median time-to-fill for a Senior Murex Developer (MX.3, front office, rates or FX) in Gurgaon was 32 calendar days from JD sign-off to accepted offer. For a Murex Functional Architect with structured products and regulatory reporting experience: 48 days. For a Calypso Technical Architect with credit derivatives and EMIR experience: 55 days. For a SimCorp Dimension Architect: 68 days.

The MX.3 version gap:

Murex MX.3 has gone through significant architectural evolution across versions. Version 3.1.26, 3.1.40, 3.1.50, and the cloud-hosted versions on AWS/Azure have different module structures, different configuration approaches, and different integration architectures. A developer whose production experience is on MX.3 3.1.26 will have a meaningful learning curve on 3.1.50 not a complete retraining, but a structured ramp period of 6–10 weeks. For upgrade programs specifically, require experience on or near the target version.

Red flag: Any vendor claiming “large Murex bench” without being able to specify the MX.3 version, the asset class coverage, and whether the experience is front office or back office within 24 hours is presenting a back-office domestic bank pool for a front-office global bank requirement. Ask all three questions before the first CV is requested.

Platform-by-Platform: Rates, Depth, and What Experience Actually Means

Murex MX.3

Rate Table:

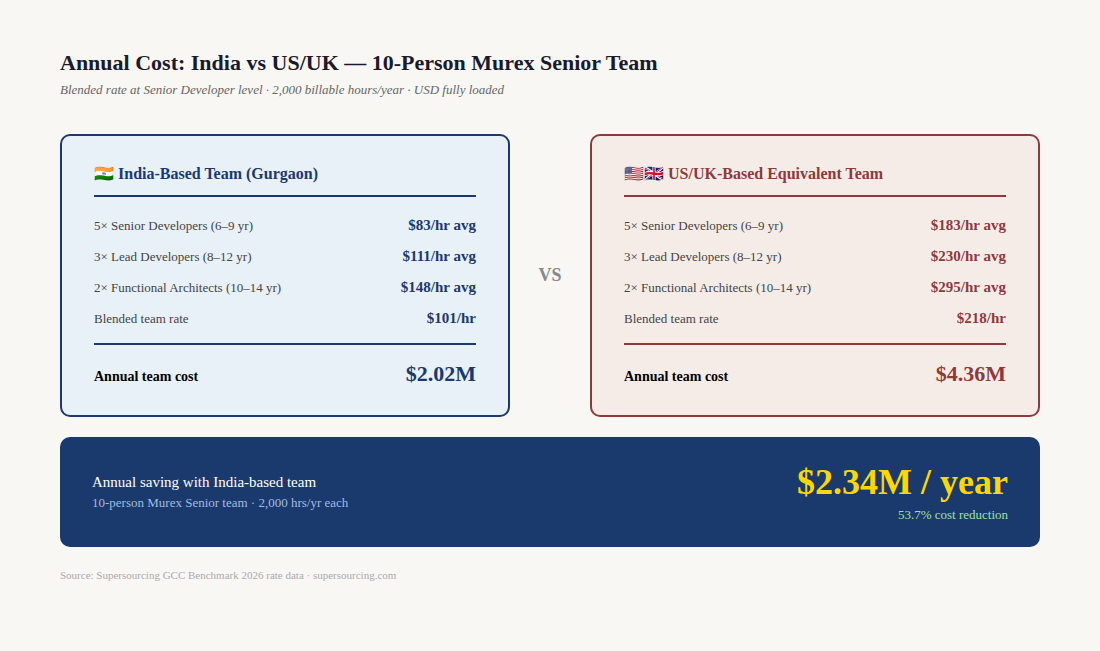

| Level | Experience | India Rate ($/hr) | US/UK Equivalent ($/hr) | Annual Saving ($) |

| Murex Developer | 3–6 yr | $45–68 | $120–160 | $156K–$192K |

| Senior Developer | 6–9 yr | $68–98 | $155–210 | $181K–$234K |

| Lead Developer / Functional Lead | 8–12 yr | $92–130 | $195–265 | $213K–$280K |

| Murex Functional Architect | 10–14 yr | $130–165 | $250–340 | $250K–$364K |

| Principal Architect / SME | 14+ yr | $155–195 | $310–420 | $322K–$468K |

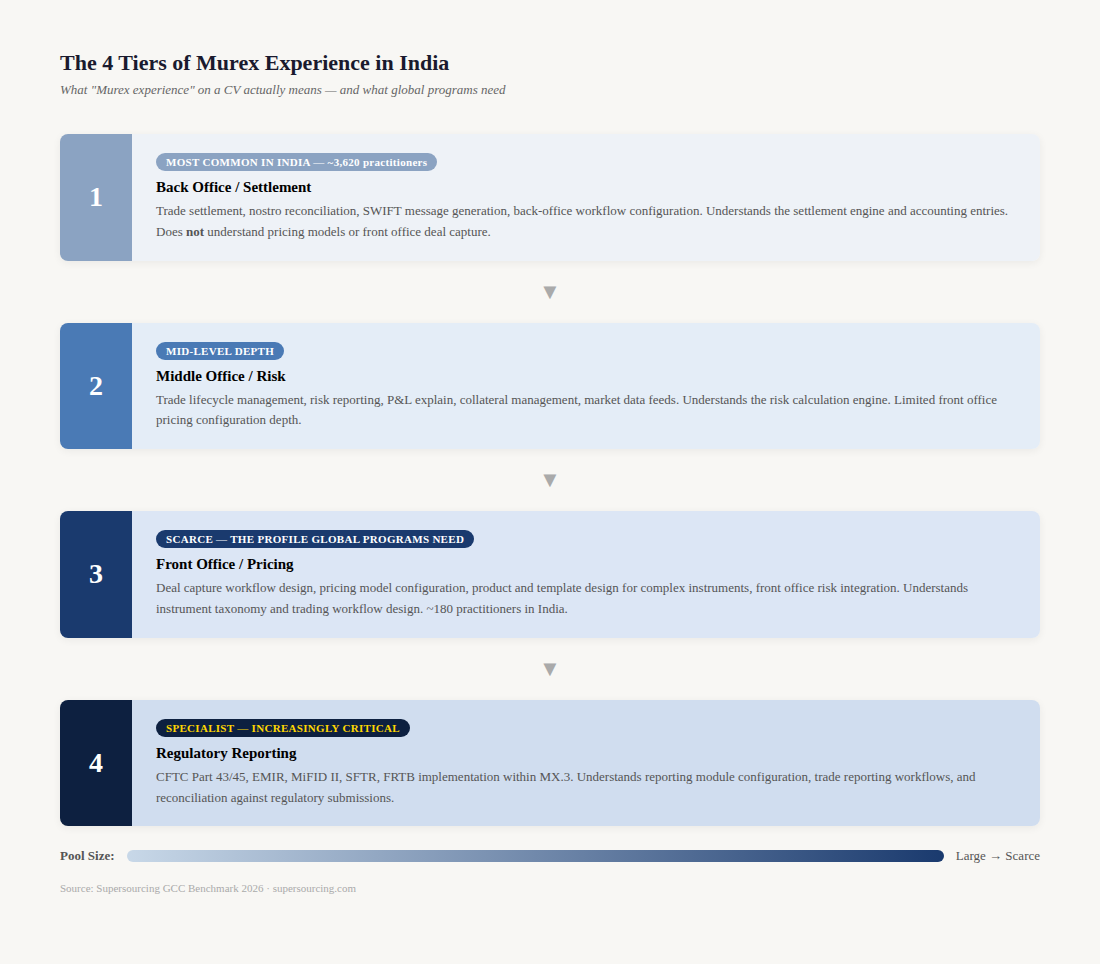

What “Murex experience” on a CV actually means the 4 tiers:

- Tier 1 Back Office / Settlement (most common in India): Trade settlement, nostro reconciliation, SWIFT message generation, back-office workflow configuration. This is the largest Murex pool in India. These developers understand Murex’s settlement engine, accounting entries, and reconciliation workflows. They do not understand pricing models, front office deal capture, or risk calculation.

- Tier 2 Middle Office / Risk (mid-level depth): Trade lifecycle management, risk reporting, P&L explain, collateral management, market data feeds. Middle office Murex practitioners understand the risk calculation engine, the market data configuration, and the P&L workflows. They have limited front office pricing configuration depth.

- Tier 3 Front Office / Pricing (scarce the profile global programs need): Deal capture workflow design, pricing model configuration, product and template design for complex instruments, front office risk integration. Front office Murex practitioners understand the instrument taxonomy, the pricing engine configuration for specific asset classes, and the trading workflow design. This is the profile that makes or breaks a capital markets Murex program.

- Tier 4 Regulatory Reporting (specialist increasingly critical): CFTC Part 43/45, EMIR, MiFID II, SFTR, FRTB implementation within MX.3. Regulatory Murex specialists understand the reporting module configuration, the trade reporting workflows, and the reconciliation against regulatory submissions. As global regulatory requirements have multiplied, this has become a standalone specialisation within Murex.

When a vendor says “Murex developer,” they almost always mean Tier 1 or Tier 2. When a global capital markets program needs Murex talent, they almost always need Tier 3 or Tier 4. Ask which tier before anything else.

The asset class matrix:

Murex experience is only meaningful in the context of which asset classes were covered. A Murex developer with rates experience has configured interest rate swap pricing, yield curve management, and rates desk workflows. A Murex developer with FX experience has configured FX spot, forward, and options pricing. These are different configurations, different pricing models, and different desk workflows. An FX developer is not automatically capable on a rates program, and vice versa.

The most common mismatch in India Murex sourcing: FX plain vanilla experience presented as rates structured products capability. Always ask for the specific asset class and instrument types covered on each project.

Calypso

Rate Table:

| Level | Experience | India Rate ($/hr) | US/UK Equivalent ($/hr) | Annual Saving ($) |

| Calypso Developer | 4–7 yr | $42–65 | $115–155 | $151K–$187K |

| Senior Developer | 7–10 yr | $65–95 | $155–210 | $187K–$239K |

| Lead / Functional Lead | 9–13 yr | $90–128 | $195–265 | $213K–$280K |

| Calypso Architect | 11–15 yr | $125–160 | $245–335 | $250K–$364K |

| Principal / SME | 15+ yr | $148–188 | $300–410 | $316K–$456K |

What “Calypso experience” on a CV actually means:

Calypso Technology (now part of ION Group) is a capital markets platform used primarily by buy-side firms, hedge funds, asset managers, insurance companies and some sell-side treasury operations. Unlike Murex which dominates sell-side trading desks, Calypso is stronger in collateral management, OTC derivatives processing, and treasury management.

India’s Calypso pool of approximately 1,400 practitioners is smaller and more concentrated than Murex. Most Calypso experience in India comes from firms like Cognizant (a major Calypso implementation partner historically) and specialist capital markets firms in Bangalore and Gurgaon.

Key distinction for Calypso: the Java customisation layer. Calypso is built on a Java framework and most enterprise implementations require significant custom Java development for workflow extensions, reporting, and integration. A Calypso functional consultant who cannot write Java is limited to configuration work. A Calypso technical developer who can both configure and extend the platform in Java is a significantly more valuable and significantly rarer profile in India.

Verify before interviewing: ask for the Java customisation depth specifically. What components have they built or extended in Java? Which Calypso APIs have they used for custom development? This single question separates functional configurators from technical developers.

Temenos T24 / Transact

Rate Table:

| Level | Experience | India Rate ($/hr) | US/UK Equivalent ($/hr) | Annual Saving ($) |

| Temenos Developer | 3–6 yr | $35–55 | $95–135 | $125K–$166K |

| Senior Developer | 6–9 yr | $55–82 | $135–180 | $166K–$202K |

| Lead / Functional Lead | 8–12 yr | $78–112 | $175–240 | $202K–$265K |

| Temenos Architect | 10–14 yr | $110–148 | $220–300 | $228K–$317K |

| Principal / SME | 14+ yr | $138–175 | $280–380 | $295K–$421K |

What “Temenos experience” on a CV actually means:

Temenos T24 (now Temenos Transact) is primarily a core banking platform, not a capital markets platform. However, Temenos has significant treasury and capital markets modules FX, money markets, derivatives, securities that are used by smaller banks and regional financial institutions.

India has approximately 2,200 Temenos-experienced practitioners, the third largest capital markets platform pool after Murex and Calypso. The pool concentrates in Chennai and Bangalore where Temenos implementation partners have established practices.

Critical distinction: Temenos core banking experience versus Temenos treasury/capital markets module experience. A Temenos developer who has worked on retail banking workflows, customer account management, and loan origination is a core banking specialist. They are not capital markets specialists. For treasury and derivatives programs, require Temenos Treasury module experience specifically, not generic “Temenos T24 experience.”

Temenos also has a formal education program Temenos Learning Community with module-specific certifications. Ask for the specific module certifications relevant to your program scope.

FIS (Front Arena / Summit / Quantum)

Rate Table:

| Level | Experience | India Rate ($/hr) | US/UK Equivalent ($/hr) | Annual Saving ($) |

| FIS Developer | 4–7 yr | $40–62 | $110–150 | $145K–$181K |

| Senior Developer | 7–10 yr | $62–92 | $150–200 | $181K–$228K |

| Lead / Functional Lead | 9–13 yr | $88–122 | $185–255 | $202K–$270K |

| FIS Architect | 11–15 yr | $118–155 | $235–320 | $239K–$337K |

| Principal / SME | 15+ yr | $142–182 | $285–395 | $296K–$442K |

What “FIS experience” on a CV actually means:

FIS has a complex product portfolio Front Arena (multi-asset front-to-back), Summit (derivatives and treasury), Quantum (fixed income), and multiple acquired products. “FIS experience” is meaningless without specifying the product. Front Arena and Summit are completely different platforms with different architectures, different user bases, and different implementation approaches.

India’s FIS pool of approximately 900 practitioners is the thinnest of the major capital markets platforms. Most FIS capital markets expertise in India comes from Wipro and Infosys delivery centers that have maintained FIS practices for global bank clients.

Front Arena specifically uses a Python-based scripting layer for extensions and customisation. Ask for the Python depth specifically. A Front Arena functional consultant without Python capability is limited to configuration. For senior roles, require demonstrated Python Front Arena extension experience.

ION Trading (Openlink / Findur)

Rate Table:

| Level | Experience | India Rate ($/hr) | US/UK Equivalent ($/hr) | Annual Saving ($) |

| ION Developer | 4–7 yr | $38–60 | $105–145 | $140K–$176K |

| Senior Developer | 7–10 yr | $60–88 | $145–195 | $176K–$218K |

| Lead / Architect | 9–13 yr | $85–120 | $180–250 | $197K–$270K |

| Principal Architect | 13+ yr | $115–152 | $230–320 | $239K–$337K |

What “ION / Openlink experience” on a CV actually means:

ION Group (which acquired Openlink and now brands the platform as Findur) is primarily used by energy trading firms, commodities traders, and some treasury departments. The India pool is approximately 480 practitioners thin and concentrated almost entirely in Bangalore and Gurgaon.

Openlink/Findur uses AVS (Avalon Script) as its primary scripting language for customisation. AVS is a proprietary language specific to the platform. A developer claiming “Openlink experience” without AVS depth is a functional user, not a developer. For technical roles, require demonstrated AVS development experience.

The commodities vs financial instruments distinction matters significantly for ION. Openlink was originally built for energy and commodities markets. Its financial instruments (FX, fixed income) coverage is functional but less deep than Murex or Calypso. Require industry context energy trading or financial markets alongside the platform experience.

The JD That Attracts the Right Candidates

JD 1: Senior Murex MX.3 Developer Rates / Fixed Income (6–9 years)

Senior Murex MX.3 Developer Rates Desk Remote from India Engagement: Staff Augmentation | Duration: 12 months, renewable Rate: ₹45–65 LPA CTC equivalent | Billing: $68–98/hr (vendor-facing)

What you’ll own: Front office Murex MX.3 configuration for our rates desk interest rate swaps, cross-currency swaps, and CMS products. You’ll work on deal capture workflow design, pricing model configuration, yield curve management, and risk reporting. This is a front office delivery role measured on trade booking accuracy, pricing model correctness, and desk workflow efficiency.

What we require:

- 6–9 years of Murex MX.3 experience, minimum 3 years on front office rates desk configuration (not back office or settlement)

- MX.3 version 3.1.40 or above specify your version experience explicitly in your application

- Rates instrument depth: interest rate swaps, cross-currency swaps, FRAs can describe pricing model configuration for each

- Yield curve configuration experience curve construction approaches, interpolation methods, curve dependencies

- Front office workflow design deal capture screens, deal validation rules, STP configuration

- Global bank experience preferred tier-1 or tier-2 investment bank, not domestic Indian bank only

What disqualifies you:

- Murex experience limited to settlement, back office, or reconciliation only

- Rates experience limited to vanilla IRS without complex product coverage

- MX.3 version below 3.1.30 as primary experience

- Domestic Indian bank only experience for a global investment bank program

Interview process: Domain screening call (30 min, rates desk context) → Live MX.3 pricing model configuration task (90 min) → Structured products architecture discussion with Front Office Technology Lead (60 min)

JD 2: Murex Functional Architect Regulatory Reporting (10+ years)

Murex Functional Architect Regulatory Reporting India GCC or BOT Engagement: GCC Build or BOT | Duration: 24+ months CTC: ₹90–130 LPA | Billing: $130–165/hr (vendor-facing)

What you’ll own: End-to-end Murex regulatory reporting architecture across CFTC Part 43/45, EMIR, and MiFID II. You will own the reporting module configuration, trade enrichment workflow design, regulatory reconciliation approach, and integration with our regulatory reporting aggregator. You will be the technical authority for a team of 8–14 Murex engineers.

What we require:

- 10+ years in Murex MX.3, minimum 4 years in regulatory reporting implementations

- CFTC or EMIR implementation experience can describe the reporting workflow from trade capture through submission and reconciliation

- MX.3 regulatory reporting module configuration trade state machine, reporting eligibility rules, UTI/UPI generation

- Integration architecture: Murex to DTCC/REGIS-TR/EMIR Trade Repository connectivity

- Multi-asset class regulatory scope rates, FX, and credit derivatives regulatory treatment differences

- Audit support experience can describe how MX.3 produces audit trail evidence for regulatory examination

Interview process: Regulatory scenario walkthrough (45 min) → Live reporting workflow design session (60 min) → Reference call with prior Chief Risk Officer or Regulatory Technology lead

What most capital markets JDs get wrong:

They say “Murex experience required” which returns the full 3,800-person India Murex pool including 10 years of back-office settlement work at domestic banks. They don’t specify the MX.3 version which means developers with Murex 2.11 experience apply for current MX.3 programs.

They don’t specify the asset class which means FX developers apply for rates programs and credit developers apply for FX programs. And they don’t distinguish front office from back office, the single most important qualification filter in capital markets hiring that most JDs completely ignore.

How to Verify Experience Not Just Credentials

Capital markets platforms Murex, Calypso, Temenos have no public certification registries comparable to Salesforce or Databricks. Murex does not maintain a public engineer certification program. This makes verification entirely dependent on structured interview technique and reference checks. The verification burden is higher than any other enterprise stack covered in this series.

The 3 verification steps before any capital markets interview:

Step 1: The Asset Class and Version Screen

Before scheduling any technical interview, ask three questions in writing:

- Which MX.3 version was your most recent production project on?

- Which asset classes and instrument types did you configure?

- Was this a front office, middle office, or back office scope?

The answers to these three questions eliminate 60–70% of mismatched candidates before a single interview is scheduled. A developer who answers “MX.3 3.1.20, FX spot and forwards, back office settlement” is not your candidate for a rates structured products front office program. No interview needed.

Step 2: The Bank Tier and Regulatory Regime Verification

Ask for the specific institution name (or “tier-1 global bank” / “tier-2 regional bank” / “domestic Indian bank” if NDA prevents naming), the geography of the trading operation, and the regulatory framework in scope. A Murex program at a global investment bank in London covers EMIR, MiFID II, and likely CFTC if the bank has US operations. A Murex program at a domestic Indian bank covers RBI regulatory requirements. These are completely different implementation contexts.

Step 3: LinkedIn and Employment History Cross-Check

Cross-check the institution names against the candidate’s LinkedIn employment history. Confirm the years of experience claimed at each institution align with the MX.3 version history if a candidate claims “MX.3 3.1.50 experience” but their employment at that institution ended before 3.1.50 was generally available, there is a timeline inconsistency worth probing.

The 5 interview questions that expose fake seniority:

Q1: Pricing Model Configuration “Walk me through how you’ve configured a CMS spread option pricing model in MX.3 the template structure, the pricing method selection, and how you handled the convexity adjustment.”

Real answer: describes the MX.3 product template structure for the CMS spread option, the pricing method selection (replication-based vs analytical), the specific convexity adjustment approach (Hull-White or SABR model selection), and how the model parameters are linked to the market data configuration. They have opinions about the tradeoffs between pricing approaches. They name specific MX.3 configuration screens.

Tutorial/back-office candidate cannot answer. Describes CMS spread options conceptually as a financial instrument but cannot describe MX.3 configuration specifics. May describe yield curve configuration generically.

Q2: Regulatory Reporting Workflow “Describe your EMIR reporting implementation in MX.3 how did you handle the UTI generation, the pairing and matching process with the counterparty, and what happened when a trade was amended post-reporting?”

Real answer: describes the UTI generation logic in MX.3 (which party generates, the format, how it’s attached to the trade), the EMIR trade repository connectivity configuration (DTCC or REGIS-TR), the pairing and matching workflow, and the amendment reporting workflow how MX.3 generates an amendment report, the action type flags, and the reconciliation process when counterparty confirmations don’t match. They describe specific MX.3 workflow states.

Tutorial/back-office candidate describes EMIR reporting requirements correctly as a regulatory framework. Cannot describe MX.3 implementation specifics. Says “the system generates the required reports.”

Q3: Market Data Configuration “How have you structured the market data configuration in MX.3 for a multi-currency rates desk yield curves, vol surfaces, and FX rates and how did you handle market data gaps and fallback logic?”

Real answer: describes the MX.3 market data feed configuration (Bloomberg or Reuters connectivity), the yield curve construction approach for each currency (bootstrapping method, instrument selection for the curve), the volatility surface configuration for rates options, and the fallback logic configuration how MX.3 handles missing data points (interpolation, previous close fallback, or error flagging). They describe the curve dependency configuration which curves feed which pricing models.

Tutorial candidate describes yield curves and volatility surfaces as financial concepts. Cannot describe MX.3 market data configuration specifics.

Q4: Trade Lifecycle and STP “Walk me through how you’ve configured STP (straight-through processing) for a vanilla IRS from front office deal capture through to settlement in MX.3 which workflow states, which validation rules, and where the most common STP breaks occur.”

Real answer: describes the MX.3 trade state machine (Simulated → Validated → Confirmed → Settled), the validation rules at each transition, the confirmation matching configuration (MarkitWire or SWIFT MT320/MT360 connectivity), and the common STP failure points missing SSI (Standard Settlement Instructions), unmatched confirmations, failed nostro account mapping and how each is handled in the workflow. They describe specific configuration items.

Tutorial/settlement-only candidate describes the IRS lifecycle as a financial concept. Cannot describe MX.3 state machine configuration or STP failure resolution.

Q5: Integration Architecture “How have you designed the MX.3 integration with a risk aggregation system? What data does Murex export, at what frequency, and how did you handle position reconciliation between Murex and the risk system?”

Real answer: describes the MX.3 export configuration (MXML export format, REST API, or direct database integration), the data elements extracted (positions, sensitivities, P&L), the extraction frequency (real-time feed vs batch), and the reconciliation approach how they handled breaks between MX.3 positions and the risk system’s view, the tolerance levels for reconciliation exceptions, and the escalation process. They name the specific risk system if NDA allows.

Tutorial candidate describes the concept of risk aggregation. Cannot describe MX.3 integration configuration or reconciliation methodology.

8 CV red flags exact language to watch for:

- “Murex experience” without specifying front office vs back office the distinction is everything

- “MX.3 experience” on a project at a domestic Indian bank for a global investment bank program different regulatory context, different instrument complexity

- “Rates experience” without naming the specific instruments IRS is very different from CMS spreads which is very different from swaptions

- “Regulatory reporting experience” without naming the specific regime CFTC, EMIR, and MiFID II are different frameworks with different MX.3 configurations

- “Calypso developer” without mentioning Java customisation depth functional configurators describe workflows, technical developers describe API calls

- “Temenos T24 experience” for a treasury program without specifying Treasury module vs core banking module

- MX.3 version below 3.1.30 as primary experience for a current MX.3 program

- “Front office experience” gained entirely in a UAT or testing capacity UAT Murex testers often describe the front office workflows they’ve tested as implementation experience

How to Source What’s Working, What Isn’t

What’s working in 2026:

GCC network referrals from existing capital markets hubs.

The Murex and Calypso practitioner community in Gurgaon and Mumbai is small and well-networked. Practitioners who leave JPMorgan’s Murex GCC know who is available at Goldman’s Murex GCC. The community is tight enough that a direct referral network outperforms job boards by a factor of 3–4x on quality. If you have existing capital markets GCC relationships in Gurgaon, ask your current team leads for referrals before opening a vendor search.

Murex and Calypso user group networks.

Murex holds annual user conferences and maintains regional user groups. The India Murex community particularly in Gurgaon has an informal network of practitioners. Direct outreach to known senior practitioners in this community produces better results than job postings. Calypso’s ION Group maintains a similar partner and user community.

3 ready-to-use LinkedIn boolean search strings:

- String 1 (Senior Murex Front Office): “Murex” AND “MX.3” AND (“front office” OR “rates” OR “derivatives”) AND (“Senior” OR “Lead” OR “Architect”) AND (“Gurgaon” OR “Mumbai”)

- String 2 (Murex Regulatory): “Murex” AND (“EMIR” OR “CFTC” OR “MiFID”) AND (“India” OR “Gurgaon” OR “Mumbai”)

- String 3 (Calypso Technical): “Calypso” AND “Java” AND (“derivatives” OR “collateral” OR “OTC”) AND “India”

Capital markets specialist staffing firms.

Unlike general IT staffing, capital markets platform staffing has specialist firms in India smaller outfits that focus exclusively on Murex, Calypso, and Temenos placements. These firms have deeper bench relationships in the community than general IT staffing vendors. For capital markets programs specifically, a specialist capital markets staffing firm will outperform a general IT staffing vendor on both quality and timeline.

Supersourcing pre-vetted bench. For Senior Murex Developers (front office, rates or FX, MX.3 current version), Supersourcing’s median fill time is 32 calendar days with pre-vetted bench including asset class and version verification before any CV is submitted.

What isn’t working:

Generic “Murex developer” postings on Naukri.

Returns the full 3,800-person India Murex pool predominantly back-office, settlement-focused, domestic bank experience. The signal-to-noise ratio is the worst of any enterprise stack. Every applicant looks like a Murex developer. 90% are not relevant for a global capital markets front office program.

Asking general IT vendors for “Murex CVs.”

General IT staffing vendors who don’t specialise in capital markets will source from their broadest Murex pool which is back-office domestic bank experience. They do not have the domain knowledge to filter for front office vs back office or for specific asset class experience. A general IT vendor for a Murex program is almost always the wrong choice.

Rate card benchmarking against general IT rates.

Capital markets platform specialists, particularly Murex front office architects, command rates that are 40–60% above general enterprise technology rates at the same experience level. A CISO who benchmarks a Murex architect rate against a Java architect rate is comparing different talent pools. The premium is real and justified by scarcity.

Interviews without domain-specific technical assessment.

A Murex interview without pricing model configuration questions is not a filter. Coached candidates can describe MX.3 trade lifecycle from documentation. The only reliable filter is a live MX.3 configuration task in a sandbox building a product template, configuring a yield curve, designing a workflow state transition. Without a live assessment, you are hiring based on description.

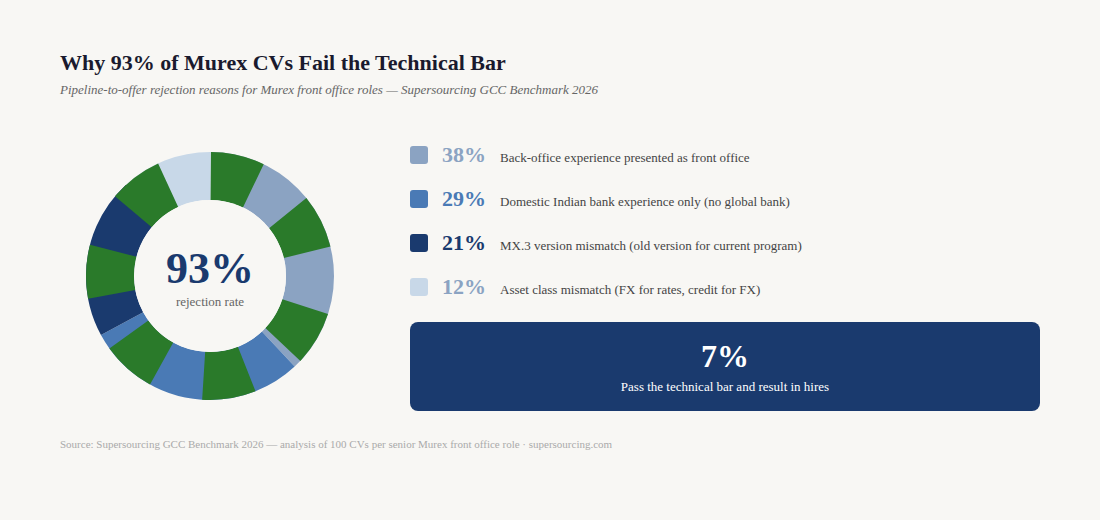

Supersourcing Index: Pipeline-to-offer conversion rate for Murex front office roles in the Supersourcing GCC Benchmark 2026: 7%. Of every 100 CVs submitted for senior Murex front office roles, 7 result in hires that pass the technical bar described in Section 7. Primary rejection reasons: back-office experience presented as front office (38%), domestic Indian bank experience only (29%), MX.3 version mismatch (21%), asset class mismatch (12%).

The Contract Stack for Capital Markets Engagements

Capital markets engagements require contractual protections beyond standard IT MSAs. Market data access, trading system access, and regulatory reporting involvement create specific IP and liability considerations.

Clause 1: Individual Resource Approval with Version and Asset Class Specification

Every engineer approved for the engagement must be listed in the SOW schedule with: name, MX.3 version experience, asset class coverage, and front/middle/back office scope. Version and asset class are contractual specifications, not preferences. An engineer substituted from rates/front office to FX/back office without client approval is a material scope change, not a personnel change.

Clause 2: Substitution Notice 21 Days for Capital Markets

Capital markets programs warrant a longer substitution notice period than standard IT 21 days rather than 14. The ramp time for a new Murex developer on a front office program is 6–8 weeks. A 14-day notice period with a 6-week ramp means 4 weeks of reduced capacity on a trading desk program. Negotiate 21 days written notice with client approval and a 30-day parallel running period where the departing engineer transfers knowledge to the replacement.

Clause 3: Market Data and Position Data Confidentiality

Capital markets program engineers have access to market-sensitive information pricing models, position data, trading strategies, and in some cases pre-trade flow information. The MSA must include an explicit market data and position data confidentiality clause covering: prohibition on using client market data or position information for any purpose outside the engagement, prohibition on sharing client trading strategies or pricing model configurations with any third party, and a post-engagement restriction period on working for direct competitors on the same trading desk technology. This is standard in capital markets vendor contracts and any vendor unwilling to sign it is a red flag.

Clause 4: IP Assignment Pricing Models and Regulatory Mappings

Pricing model configurations in Murex particularly for bespoke structured products are proprietary IP. The IP Assignment Deed must explicitly cover: custom MX.3 product templates and pricing model configurations, custom regulatory reporting mapping logic, custom workflow scripts and calculations, and any trade data transformation logic developed for the engagement. These items are not obviously “software code” under standard IP clauses.

Clause 5: Trading System Access Revocation 2 Hours

For engineers with access to production Murex environments, particularly front office environments connected to live pricing feeds, access revocation must be faster than standard IT programs. Require production Murex environment access revocation within 2 hours of engagement end notification. For development and UAT environments: 24 hours is acceptable.

Clause 6: Regulatory Liability Limitation

For engagements where the offshore team is implementing regulatory reporting CFTC, EMIR, MiFID II include an explicit clause defining the boundary of regulatory liability. The vendor’s engineers are implementing based on your specifications.

Regulatory reporting errors that result from specification changes, market data quality issues, or regulatory interpretation decisions made by your compliance team are your liability, not the vendor’s. Errors resulting from implementation mistakes against agreed specifications are the vendor’s liability. This boundary needs to be explicit regulatory reporting penalties are material and the liability allocation matters.

Running a Capital Markets Team at Scale

Governance model for a 10–20 engineer capital markets program:

Domain knowledge pairing.

Every offshore Murex engineer should be paired with an onshore or near-shore business analyst or functional expert who owns the domain requirements. Capital markets programs fail when offshore engineers interpret ambiguous trading requirements without a domain-knowledgeable counterpart to validate. The dedicated development team implements. The onshore BA or functional expert validates against business intent.

MX.3 environment governance.

Production, UAT, and development environments must be strictly separated with formal promotion processes. A configuration change in development that affects pricing model behaviour must go through UAT validation including front office sign-off from the trading desk before production promotion. Offshore engineers should have development and UAT access. Production access should be limited to a named lead with dual approval from your internal technology team.

Version control for MX.3 configurations.

MX.3 configurations product templates, pricing model parameters, workflow definitions must be version-controlled. Murex provides configuration export mechanisms. All configuration changes should be exported, version-controlled in Git, and peer-reviewed before UAT promotion. A capital markets program without configuration version control cannot audit configuration changes, cannot roll back pricing model errors, and cannot produce the change history that regulators require.

Model validation ownership.

Pricing model configurations in MX.3 must be validated by your quant or model validation team before production deployment. Offshore engineers configure the model. Your internal quants validate it. This is non-negotiable for any front office program; a misconfigured pricing model produces incorrect marks that affect P&L, risk, and potentially regulatory reporting.

Early warning signals that a capital markets engineer is disengaging:

- Declining configuration quality incomplete product templates, missing validation rules

- Slower response to desk queries trading desk questions taking hours instead of minutes

- Missed model validation sessions configuration submitted to quants without attending the review

- LinkedIn activity capital markets platform skills updated, connections from competing banks

- Increasing configuration errors in UAT that were not present in earlier sprints

Retention levers specific to capital markets engineers in India:

Asset class expansion keeps them. A Murex developer who starts on vanilla IRS and gets exposure to CMS spreads, then swaptions, then exotics is building a career story. Asset class breadth is the primary career development lever in capital markets technology. Engineers who expand their instrument coverage on your program are not looking for the door.

Regulatory complexity is a retention mechanism. CFTC, EMIR, MiFID II, FRTB regulatory programs give capital markets engineers exposure to global regulatory frameworks that are valuable and portable career credentials. Engineers who own a regulatory workstream stay through the program because departure mid-regulatory implementation is a career risk they won’t take.

Global bank exposure is worth more than salary. For an Indian capital markets engineer, having a global tier-1 investment bank on their CV is worth a 25–30% salary premium in their next role. Engineers on your program know this. They stay because the association is valuable. Acknowledge it “you’re building a global bank CV” is a genuine retention message in this community.

When Things Go Wrong

Pattern 1: The Back Office Masquerade

Described in Section 1. The NASDAQ-listed P&C insurer story from Guide 1 in this series was also a version of this pattern. A vendor presents Murex developers with genuine MX.3 experience just not the right tier. Back-office settlement experience is presented as front-office capability. The gap only emerges when the trading desk asks questions that settlement developers cannot answer.

The fix in all cases was the same: the asset class and desk tier screening in Section 7. Three questions before the first interview eliminate this pattern entirely.

Pattern 2: The Regulatory Deadline Miss

A European investment bank EMIR refit deadline looming hired 6 Murex engineers for regulatory reporting. The vendor presented experienced Murex developers. None had EMIR implementation experience, specifically their regulatory reporting background was RBI reporting for domestic Indian banks.

RBI regulatory reporting and EMIR reporting use completely different MX.3 modules, different report formats, different trade repository connectivity, and different UTI generation logic. The India team was learning EMIR from documentation while the deadline clock ran.

The bank missed the EMIR refit deadline by 6 weeks. FCA inquiry. £180K fine. The offshore team was not at fault; they learned and delivered. The timeline assumption that domestic Indian regulatory experience transfers to EMIR was the buyer’s mistake.

The verification fix: ask specifically which regulatory regime and which trade repository. DTCC vs REGIS-TR vs ESMA portal experience are verifiable specifics that distinguish EMIR practitioners from domestic regulatory practitioners.

Pattern 3: The Version Cliff

A US-based asset manager running Calypso on an older version hired an offshore team to extend the platform for new instrument types. The vendor’s Calypso engineers had current version experience Calypso 14.x. The client’s production environment was Calypso 11.x.

The API changes between Calypso 11.x and 14.x were substantial. The custom Java components the offshore team built against 14.x APIs did not compile against the client’s 11.x environment. Four months of development work required significant rework for version compatibility.

The fix: specify the exact platform version in the JD and SOW schedule. Make version-specific experience a contractual requirement, not a preference. A Calypso 14.x engineer on an 11.x program has the same problem as an XM Cloud Sitecore developer on an XP 9.3 program with a different API layer, different configuration model, different debugging context.

When India Is the Wrong Call

Three scenarios where India-based capital markets hiring creates more risk than value.

Scenario 1: Real-time trading desk support with sub-second latency requirements.

If your program requires engineers who are available on a trading desk during market hours New York or London trading hours for real-time support of live pricing and execution systems, the India timezone creates an operational constraint that is difficult to manage. IST UTC+5:30 means India morning covers early European market open and India evening covers US market open, but the core US afternoon session (2pm–4pm EST) falls at midnight in India. For production support of live trading systems during core market hours, consider EMEA or Americas-based engineers for the L1/L2 support layer with India-based engineers for development and L3 resolution.

Scenario 2: Highly bespoke exotic derivatives with no India precedent.

For the most complex structured products digital barriers, auto-callables, multi-asset baskets with path-dependent payoffs the MX.3 configuration depth in India thins significantly. India’s capital markets talent pool has deep experience on vanilla and standard structured products. For truly exotic instruments that a small number of tier-1 banks trade, the practitioners who have configured MX.3 for those specific products may not be in India. For these cases, consider a hybrid model: onshore quant and SME for exotic instrument configuration design, offshore India team for vanilla and semi-complex instrument configuration and back-office work.

Scenario 3: FRTB implementation with model approval requirements.

The Fundamental Review of the Trading Book (FRTB) is the most complex regulatory capital program in current capital markets technology. FRTB IMA (Internal Models Approach) implementation requires regulatory approval of the risk models themselves, not just the technology implementation. The model governance, documentation, and regulatory interaction components of FRTB require practitioners with deep regulatory relationships and model validation experience that is concentrated in London, New York, and Frankfurt not India. India-based engineers can implement the technology layer of FRTB. The model governance and regulatory approval process requires onshore or near-shore expertise.

The Supersourcing Vendor Scorecard Capital Markets Edition

Score your vendor before you sign. Maximum 100 points. Minimum threshold to proceed: 70. Capital markets programs warrant the highest threshold of any guide in this series.

Category 1: Bench Depth and Domain Specificity (0–20 pts)

| Criterion | 0 | 10 | 20 |

| Can specify asset class and desk tier for all claimed bench within 24 hours | Cannot | Some | All bench, all specified |

| Front office practitioners available (not back office only) | None | 1–2 | 3+ verified front office |

| MX.3 version currency (3.1.40 or above) for claimed bench | Below 3.1.30 | Mixed versions | All 3.1.40+ |

Category 2: Domain Vetting Process (0–20 pts)

| Criterion | 0 | 10 | 20 |

| Asset class specific technical assessment | Generic Murex questions | Asset class specific written | Live MX.3 sandbox task |

| Regulatory regime verification in technical screen | None | Generic regulatory questions | Regime-specific workflow questions |

| Reference from a named global bank (not domestic only) | None | Domestic bank only | Named global bank reference |

Category 3: Contract Readiness (0–20 pts)

| Criterion | 0 | 10 | 20 |

| IP Assignment covering pricing model configurations and regulatory mappings | Not available | Available on request | Standard, items named specifically |

| Market data and position data confidentiality clause | Not present | Present, vague | Present, specific prohibitions listed |

| Trading system access revocation 2 hours for production | Not present | 24 hours | 2 hours, production specifically |

Category 4: Capital Markets Delivery Track Record (0–20 pts)

| Criterion | 0 | 10 | 20 |

| Named global bank Murex clients they can reference | None | Logo only | Named contact at global bank |

| Completed front office programs verifiable asset class | None claimed | Claimed, unverified | Verified with asset class and go-live |

| Attrition on capital markets programs | Unknown / >15% | 10–15% | <10% |

Category 5: Commercial Structure (0–20 pts)

| Criterion | 0 | 10 | 20 |

| Rate card by asset class tier and front/back office | Single rate | Front/back distinction | Full tier and asset class matrix |

| Substitution clause with 21-day notice and parallel running | Not present | 14 days | 21 days with parallel running |

| Domain-specific SLA on replacement | None | Best effort | Contractual SLA ≤21 days with asset class equivalence |

Score interpretation:

- 85–100: Shortlist. Proceed to SOW negotiation.

- 70–84: Proceed with conditions. Close Category 1 and 2 gaps before signing.

- 50–69: Significant risk. A capital markets vendor below 70 will almost certainly produce a back-office team for a front-office requirement.

- Below 50: Walk. The remediation cost of a failed capital markets engagement exceeds the cost of finding the right vendor.

15 Questions Buyers Actually Ask

Q: What’s the difference between a front office and back office Murex developer?

Front office Murex developers configure the trading and pricing layer deal capture workflows, pricing model configuration, yield curves, volatility surfaces, and front office risk integration. They work directly with trading desks and quants. Back office Murex developers configure the settlement and accounting layer trade settlement workflows, nostro reconciliation, SWIFT connectivity, accounting entries, and back-office reporting. Both are legitimate Murex specialisations. They require completely different skills, and a back-office developer cannot perform front-office work without significant retraining. Always specify which you need before the first CV is requested.

Q: Does Murex have a certification program I can use for verification?

No, Murex does not maintain a public certification program comparable to Salesforce or Databricks. Murex provides training courses and internal competency assessments through Murex University, but these are not independently verifiable against a public registry. Verification for Murex is entirely dependent on: the structured interview questions in Section 7, reference checks with named global bank clients, and live MX.3 sandbox assessments. This makes Murex one of the hardest platforms to verify in enterprise staffing and one of the most frequently misrepresented.

Q: Can I hire Calypso developers to supplement a Murex program?

Not directly. Murex and Calypso are different platforms with different architectures, different data models, and different scripting languages. A Calypso developer cannot configure MX.3 without starting from scratch. The only transferable skills are domain knowledge, understanding of derivatives, regulatory frameworks, and capital markets workflows which is valuable context but not implementation capability. For a mixed-platform program, hire platform-specific for each system.

Q: What’s the realistic timeline to build a 15-person India Murex team?

For a front-office focused team rates, FX, structured products, regulatory expect 55–70 days from JD sign-off to full 15-person team accepted and onboarded. The front-office pool is thin (approximately 180 practitioners at senior level in India), the asset class specificity narrows it further, and the version requirement narrows it again. For a back-office or settlement-focused team, the timeline is significantly shorter 30–45 days because the pool is larger and the verification requirements are less intensive.

Q: How do MX.3 version upgrades affect the India talent pool?

Significantly. Each major MX.3 version introduces new modules, new configuration approaches, and architectural changes. Engineers whose primary experience is on MX.3 3.1.26 will have a 6–10 week ramp on 3.1.50 even for experienced practitioners. For upgrade programs specifically where version familiarity is the primary delivery value require experience on or within one major version of the target. Accepting a two-version gap on an upgrade program adds ramp time that effectively extends your timeline by the ramp period.

Q: Is there a FRTB Murex specialist pool in India?

Yes small and concentrated. FRTB IMA and SA implementations in MX.3 have been delivered by tier-1 bank India GCCs from 2022 onwards. The practitioners who have worked on FRTB MX.3 implementations at JPMorgan, Goldman, or HSBC India GCCs have directly transferable experience. The pool has approximately 60–80 practitioners in India. Median fill time for a FRTB Murex Architect: 55+ days. Rates at the top of the architect range. Competition from tier-1 banks for the same profiles.

Q: Can I use a BOT model for a capital markets Murex GCC?

Yes and several tier-2 and regional banks have done exactly this. The BOT model works well for Murex GCCs when the transfer clause specifies that the MX.3 configuration knowledge configuration documentation, product templates, pricing model specifications, regulatory mapping logic transfers alongside the headcount. A Murex GCC where the institutional knowledge lives in the vendor team and not in documented artifacts is a failed BOT regardless of the headcount transfer. Guide 2 in this series covers BOT transfer clause specifics.

Q: What’s the difference between Murex and Bloomberg AIM/TOMS for hire purposes?

Murex MX.3 is a full-cycle trading system front office, risk, and back office used primarily by dealer banks (sell-side). Bloomberg AIM (Asset and Investment Manager) and TOMS (Trading Order Management System) are buy-side order management systems used by asset managers and hedge funds. They serve different market participants, have different functional scopes, and require practitioners from different career backgrounds. A Murex developer from a dealer bank background is not automatically equipped for Bloomberg AIM at a hedge fund, and vice versa. Specify the platform and the institution type when briefing vendors.

Q: Is India-based Murex talent comparable to UK and US talent in quality?

At senior level for standard and semi-complex instrument types: yes, functionally equivalent for implementation roles. India’s Murex community has delivered front-office programs for tier-1 banks for 15+ years. For the most exotic and complex structured products, the deepest Murex expertise remains concentrated in London, New York, and Paris where the products were invented and the banks that trade them are headquartered. For vanilla, standard structured products, and regulatory reporting: India-based Murex talent delivers at global quality standards. For ultra-exotic structured products at tier-1 banks: consider onshore SME for product design and offshore India team for implementation.

Q: How do I structure the interview process for a Murex architect role?

Three stages: domain screening (30 minutes asset class, version, desk tier), technical assessment (90 minutes live MX.3 sandbox task relevant to your specific instrument types), and SME reference call (30 minutes your internal quant or front office technology lead speaks directly with a prior client reference). The reference call is non-negotiable for architect roles in capital markets. A candidate who cannot provide a reference from a named global bank program for an architect role has not delivered at that level.

Q: What’s the hardest capital markets profile to hire from India in 2026?

A SimCorp Dimension Architect with IBOR/ABOR conversion and AIFMD/UCITS regulatory reporting experience. SimCorp is used by asset managers and institutional investors in a smaller market than sell-side platforms. The India SimCorp pool has approximately 320 practitioners with approximately 45 at architect level. IBOR (Investment Book of Records) to ABOR (Accounting Book of Records) conversion is a specific SimCorp program type with very few practitioners who have delivered it. Median fill time: 68 days. Rates at the top of the architect range.

Q: Can one vendor handle both Murex front office and regulatory reporting on the same program?

Yes but require separate CV verification for each workstream. Front office configuration and regulatory reporting are different Murex specialisations. A vendor who claims depth on both should produce separate references for each: a trading desk technology reference for front office capability and a regulatory technology or compliance reference for the reporting capability. Bundling both in a single rate card without verifying each workstream separately is how you get a front-office team that can’t build a CFTC report.

Q: Is Supersourcing the right partner for a 3-developer Murex program?

Not our ideal engagement. Our model is built for 8+ engineer programs with enterprise governance and SOW-level accountability. For 3 Murex developers on a defined scope, a capital markets specialist staffing firm with deep Murex community relationships is a better fit. We’d rather tell you that than win a deal we’ll underserve.

Q: How does data residency affect India-based capital markets programs?

Market data Bloomberg or Reuters real-time feeds and position data are subject to data residency considerations in some regulatory jurisdictions. For US programs: CFTC regulations on trade data residency may affect where certain trade data can be stored or processed. For EU programs: GDPR and EMIR data residency requirements may constrain where trade data flows. Work with your compliance team to define which data categories can flow to India-based engineers, which require data masking or anonymisation, and which require access via a VPN into your local environment rather than data transfer. Most capital markets programs manage this through environment access (offshore engineers access systems in your jurisdiction via VPN) rather than data export.

Q: What’s the most commonly overlooked cost in India Murex hiring?

The ramp costs the period between an engineer’s start date and when they are fully productive depending on your specific MX.3 environment, instrument set, and program context. For a front-office Murex engineer joining a complex structured products program, the ramp to full productivity is 6–10 weeks even for a genuinely senior practitioner. This ramp cost billing hours at full rate for 60–70% productivity is real and should be factored into the economic model. A 10-person Murex team with a 8-week average ramp costs approximately $300K in ramp inefficiency at senior rates. Reduce it with a structured onboarding program, documented MX.3 configurations, and a named buddy from your internal team for each offshore engineer.

Closing

Murex and capital markets platform hiring from India works. The front-office Murex talent is real, the global bank delivery track record is deep, and the savings versus UK and US hiring are substantial $181K to $468K per engineer per year depending on level.

The failure mode is not India. The failure mode is hiring “Murex experience” when you need “MX.3 3.1.50 front office rates structured products experience.” It is accepting a domestic Indian bank reference for a global investment bank program. It is signing an MSA without an asset class specification in the resource approval clause.

The verification questions in Section 7 take 15 minutes. They eliminate the 93% of submitted CVs that won’t pass the technical bar. The 7% that remain are the ones who have built what you need. They exist in India. Finding them requires the right questions, not the right job board.

If you want Supersourcing to verify a specific capital markets role, bring us the platform, the asset class, the MX.3 version, and the regulatory scope. We’ll tell you what the talent pool looks like, what the realistic rate is, and how long it will take to source someone who passes every layer.

Book a 30-minute Capital Markets Talent Discovery Call → No deck. Just the numbers and the bench.